The extent of the damage is now known. Recently-published statistics from the Federation of the Swiss Watch Industry (FH) report a fall in exports for 2009 of 22.3%, at CHF 13.23 billion ($12.17 billion). “Such a marked decline means it was a particularly harsh year for certain brands, and for suppliers as a whole,” comments Jean-Daniel Pasche, President of the FH. “Watchmaking has lost almost a quarter from year to year. However, we do need to analyse these figures with caution, as they do not reflect sales to end customers.”

Still, never before has sell-out been the focus of such attention, as the branch looks anxiously at retailer inventory in the different markets. In the absence of precise sales figures from the brands themselves, FH statistics give a global view of the situation and sketch in the changes that took place over this crucial year. Summary below.

Year-end upturn: The shift from a double-digit to a single-digit decline in November (-10.6%) was confirmed in December (-7.2%). According to René Weber, an analyst with Vontobel, this positive note is due mainly to the base effect. The Asian markets also showed definite signs of recovery, particularly Hong Kong and China. “We were expecting an improvement at year-end and this is what we’ve seen,” declared a relieved Jean-Daniel Pasche.

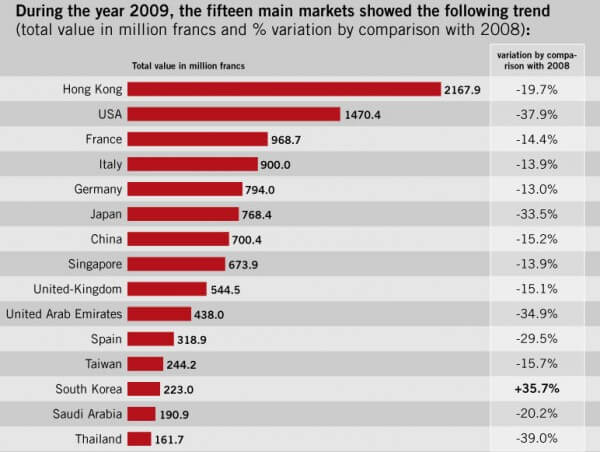

Asia I: In terms of growth, the Asian markets are taking over from the flagging mature markets. The United States, for example, dropped 38% on 2008. “We hope that Asia will pull other regions along in its wake, particularly the US where we are clearly seeing the first signs of a pick-up in consumption, although this hasn’t yet spilled over into exports,” Jean-Daniel Pasche rues.

Asia II: Officially, the Asian continent accounts for 48% of Swiss watch exports (+10 percentage points in two years). “If we also include Asian tourists who buy watches when on holiday, we can estimate that over two-thirds of Swiss watches sold worldwide go back to Asia,” watch consultant Olivier Müller observes. Still marginal markets such as India represent huge growth potential, which should push sales up over the coming years.

Suppliers: The drop in orders with suppliers is probably more than proportional to the actual downturn in the market. “This is what’s known as the bullwhip effect,” Olivier Müller explains. “It’s a lever effect that works both ways, whereby market players across the chain, from supplier to retailer, anticipate fluctuations in demand.”

2006 level: Ultimately, 2009 ended less badly than it began, when the initial trend was for a downturn closer to 30%. The upturn in the fourth quarter means the year ended on a par with 2006, a record year, let it be said, as were 2007 and 2008. Compared with 2003, the last recorded recessive year, 2009 posted a 30% increase.

Prices down: The 6% fall in average price is more surprising, coming after cumulative and uninterrupted inflation of almost 50% since 2004 and a 17% drop in exports in volume terms. For Jean-Daniel Pasche, this means luxury watches have been harder hit than other segments, “Although we do need to put these figures into perspective,” he notes. “Because the high end of the market progressed the most during the extravagant years of 2004-2008, it has the handicap of an unfavourable base effect compared with the mid-range.”

Beyond the figures published by this umbrella organisation, wider observations can be made.

- Disparities: The crisis has hit brands to very different degrees. Some of the heavyweights, such as Omega and Cartier, have weathered the storm well, while others have seen sales slide by between -30% and -45%, sometimes more. For those brands that are heavily exposed in America, 2009 was a particularly tricky year.

- Domino effect: Small brands have suffered more than their share of recession. They rode out the first months thanks to orders taken in 2008 that were delivered in 2009. “Financially speaking, many of these brands have been bled dry. After using and abusing supplier credit, and causing substantial damage to contractors in the process, all they can hope for now is that the market turns round,” Olivier Müller observes.

- Legitimacy: Consumers are making safe investments and buying watches from established, enduring brands. Which hasn’t prevented these same brands from agreeing to discounts to push sell-out. Says Olivier Müller, “Brands will face the same challenge: keep control of supply upstream and distribution downstream.”

So how does this bode for the current year? “We expect this improvement to continue for the coming months, with a subsequent increase in exports in 2010,” forecasts Jean-Daniel Pasche. “The big issue at the moment is stock reduction, which probably hasn’t reached its end.”