An excellent first half for luxury brands

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

The year has got off to a resounding start for publicly-traded luxury companies, with double-digit growth and a strong outlook for the full twelve months. For watch companies, it’s a similarly rosy picture.

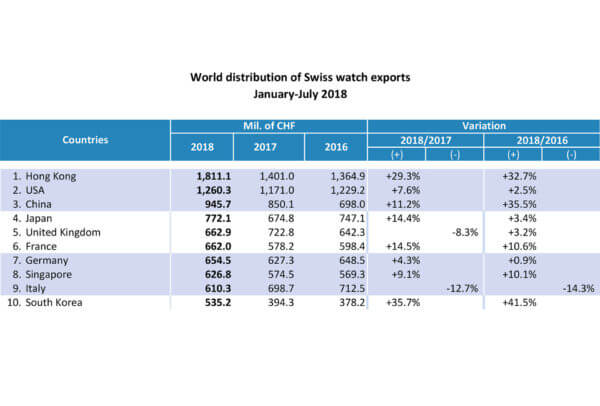

After a gloomy 2015-2017 that chipped away at the Swiss watch industry, particularly in 2016 when exports lost 10%, happy days are here again. First off, the luxury industry in general has reported a strong first half for 2018. For the watch sector in particular, the upswing that began during the second half of 2017 (+4.9%) has carried on into this year. Numbers published by the Federation of the Swiss Watch Industry show that, for the first seven months of 2018, exports posted a solid 10% increase. Of the twenty main markets, the only notable declines have been in one or two European countries, starting with the United Kingdom (-8.3%) where the potential fallout from Brexit poses bigger threats than the devaluation of sterling, which had the effect of boosting sales. This aside, the main markets, for example Hong Kong (+29.3%) and even the USA (+7.6%), are forging ahead.

Prior to publication by Richemont of five-month results at its annual general meeting on September 10th, Swatch Group figures are sufficiently eloquent. The world’s biggest watch group has reported a record first-half 2018, corresponding to an increase in sales of 14.7% to CHF 4.2 billion. Operating result increased 69.5% to CHF 629 million. Operating margin is similarly upbeat, improving from 10% in 2017 to just under 15%. Market capitalisation has followed the same upward trend; over one year to end August, shares in the group gained close to 15%.

LVMH and Kering see share prices surge

Across the Alps from Switzerland, France’s luxury players have sustained an equally impressive performance. Hermès, which recorded an 11% rise in first-half revenue at constant exchange rates (+5% at current rates), has seen its share price leap by 25% over the past six months. After struggling in recent years, its watch business has gained in substance as sales climbed 9% to €77 million between January and June 2018. The company has high hopes in terms of profitability and forecasts an operating margin comparable to the 34.4% of last year. It’s a similar picture for LVMH’s Watches & Jewelry division, albeit with significantly larger volumes. The business group, which includes Hublot, TAG Heuer, Zenith and Bulgari, generated just short of €2 billion (+8%) in revenue over the six months in question. Profit from recurring operations shot up by 46% to €342 million. LVMH shares have gained 40% in one year.

Kering has its share of good news, too. Commenting on the group’s half-year numbers, Chairman and CEO François-Henri Pinault had this to say: “Kering achieved dazzling top-line and earnings performances in the quarter and six months. Our growth, grounded in the exclusivity and desirability of our brands, is remarkably healthy.” The 26.8% increase in revenue over six months was driven by exceptionally strong figures from Gucci (+36% to €3.8 billion), which already sees itself toppling Louis Vuitton from the world’s number-one luxury brand spot by lifting revenue to €10 billion in the short- to medium term. Kering’s Other Houses, which include watchmakers Ulysse Nardin and Girard-Perregaux alongside Boucheron, Balenciaga and Alexander McQueen, progressed by 31.1% to €995.5 million. Over 12 months, Kering shares have shot up by 65%. No-one would dare describe this recovery as “timid”, even in the context of an escalating trade war between Washington and the rest of the world.

{kind=link}

{kind=link}

{kind=link}

{kind=link}