Richemont’s five glorious years

Open Gallery

The Vacheron Constantin Manufacture in Plan-les-Ouates, Switzerland © Vacheron Constantin

In the space of five years, Richemont has doubled both sales and profit. The Geneva-based luxury group, established 25 years ago, sees this as just a taste of things to come.

When Johann Rupert, chairman of the Richemont Group, begins his sabbatical he can do so with the satisfaction of a job well done. The Group sits on solid foundations, results exceed all expectations, and the outlook is dazzlingly bright, even if blips in the economy can never be ruled out. Imagine the hard work, tenacity and self-sacrifice to the point that the head of the world’s second-biggest luxury group felt the need to take a break and expand his horizons. As he explained at a conference call with analysts, the decision to take this gap year came when he realised his diary was booked twelve months in advance. Just one example: when a friend suggested they go watch the Rugby World Cup together, Rupert had to decline the invitation for the simple reason he had too many meetings planned. One thing is for sure: Johann Rupert will return to business refreshed and more dynamic than ever. In a year’s time. A year that will doubtless fly by.

Welcome to the third dimension

A look at the past five years reveals the extent to which the Group, which is headquartered in Bellevue in the canton of Geneva, has taken on a new dimension and entered a new era. Granted, like others in the luxury sector it has benefited from rising demand for quality products and the voracious appetite of emerging countries, led by Asia, for this type of good. However, few luxury names post results that push the needle off the scale. In five short years, Richemont’s sales and profits have virtually doubled. Sales have climbed from EUR 5.418bn to EUR 10.150bn, an increase of 87%. Jewellery now accounts for 51% of Group sales, watches 27%, Montblanc 8% and other activities 14%. The Asia-Pacific region paints an even rosier picture as sales rocketed to EUR 4.16bn from EUR 1.47bn in 2009. Last year, China and Hong Kong alone recorded EUR 2.6bn in sales.

Net profit is on the same upward trajectory. From EUR 1.07bn in 2009, it climbed to EUR 2.005bn for the 2012-13 financial year to March 31st. Even more impressive, operating profit for the Group, which owns the likes of Cartier, IWC, A. Lange & Söhne, Panerai and Jaeger-LeCoultre, has soared, rising from EUR 968mn to EUR 2.426bn in the last financial year. This equates to a 150% increase with an operating margin of 24%. Operating margin for the Group’s jewellery division reached a vertiginous 35%. Twice that of Nestlé.

Over a thousand stores

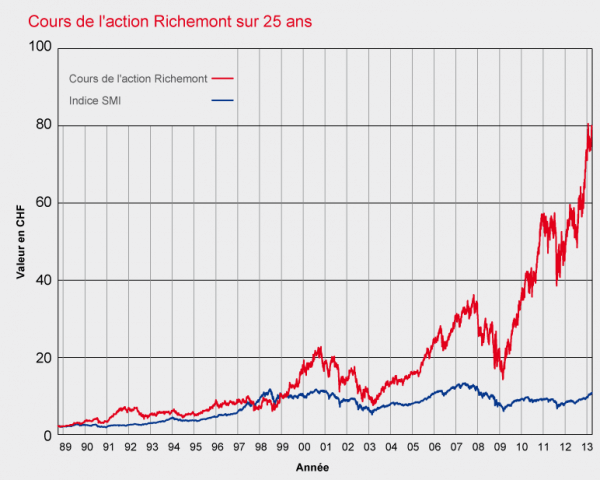

To use a bold comparison, Richemont is an empire on which the sun never sets, from a retail stance at least. The Group heads a global network of over a thousand wholly-owned or franchised monobrand stores for its Maisons, which include Roger Dubuis, Piaget and Van Cleef & Arpels. The Group makes 54% of total sales through these stores, the remaining 46% coming from retailers. The balance could well sway further towards the monobrand network, where sales grew 17% last year compared with 12% in the retail network, which five years ago weighed 54% in the Group’s accounts. Shares have enjoyed similar fortunes. Over 25 years, adjusted for share splits and a major reorganisation of the Group’s activities in 2008 with the separation of its luxury and tobacco operations, they have gone from CHF 2.20 on October 12th 1988 to CHF 74.50 at March 31st 2013. Not so long ago, Richemont’s share price hit an all-time high of CHF 93.10 on the Swiss stock exchange.

A quarter-century of transformations

While the past five years have been exceptional in every way, there can be no denying that the Group sowed the seeds of success well before. In Richemont’s 2012-13 annual report, Johann Rupert looks back on the high points of a 25-year odyssey. Over three pages, he records the milestones in Richemont’s history, beginning with the establishment of the Rembrandt Group in South Africa by Dr Anton Rupert. It held interests in tobacco, financial services, wines and spirits, gold and diamond mining and, significantly, luxury goods. Richemont originated with the spin-off of its non-South African assets. In September 1988, Compagnie Financière Richemont was founded in Zug, Switzerland. At that time, it held minority investments in Cartier Monde (47%) and Rothmans International (30%), the latter having interests in Cartier and Alfred Dunhill, which itself had interests in Montblanc and Chloé. Listed on the Zurich stock exchange, the Group had Johann Rupert as chief executive officer, a market capitalisation of CHF 2.9bn, and presented its financial statements in sterling.

The following year, 1989, Richemont bought out Philip Morris’ 30% stake in Rothmans. In a first major restructuring in 1993, Rothmans was separated from the Group’s luxury businesses which became the Vendôme Luxury Group (VLG). This new group encompassed Cartier, Chloé, Karl Lagerfeld, Sulka, Montblanc, Baume & Mercier, Piaget, Dunhill and Hackett. In 1994, the prestigious gunmaker Purdey joined the Richemont stable. Financial diversification continued with the acquisition of a 15% stake in Canal+. In 1999 this was exchanged for a 3% interest in Vivendi, which the Group disposed of in a profitable transaction.

On the watchmaking side, the Group added Vacheron Constantin to its portfolio in 1996, followed a year later by Officine Panerai. It also continued to consolidate and expand its tobacco interests. In 1998, Richemont made a successful offer for the remaining 30% of VLG. Rothmans merged with British American Tobacco. Richemont, which held 35% of what had become the world’s second-largest tobacco group, decided to further develop its luxury business. It acquired 60% of Van Cleef & Arpels, increasing its stakeholding to 100% in 2003. The year before, Richemont had moved its head office to Geneva. The acquisition of Les Manufactures Horlogères from Mannesmann brought Jaeger-LeCoultre, IWC and Lange & Söhne into the fold, for an investment of CHF 3.08bn. As the Group announced at the time, “the acquisition represents a major strategic step for Richemont and will strengthen its position as one of the world’s leading manufacturers of quality watches.” Never a truer word was spoken.

"A marathon of successive sprints"

In 2008, the Group separated its interests into a luxury division in Switzerland and an investment vehicle, Reinet, in Luxembourg which held the remaining shares in BAT. Also in 2008, Richemont opened its new head office in Bellevue, a stone’s throw from Geneva. The Group continued to expand its business: in 2007 it took a stake in the Azzedine Alaïa fashion house and in 2010 acquired a controlling stake in Net-à-Porter.com, the premier online fashion retailer. Watch manufacturer Minerva, Roger Dubuis, and case-maker Donzé-Baume were also among the companies to swell its ranks.

“A marathon of successive sprints,” is how Johann Rupert describes Richemont’s first 25 years. Which is exactly the impression this quarter-century of growth, transformation and vertical integration gives. But as Rupert is quick to add, “Richemont’s history does not end here.” Meaning the best is yet to come. He then quotes Vacheron Constantin, one of the Group’s Maisons, whose precept is to “do better if possible, and that is always possible.” Quite an agenda for joint chief executive officers Richard Lepeu and Bernard Fornas thanks to whom Johann Rupert should be able to rest easy during his well-earned year off.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}