Swatch and Richemont, two different equity stories

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

Open Gallery

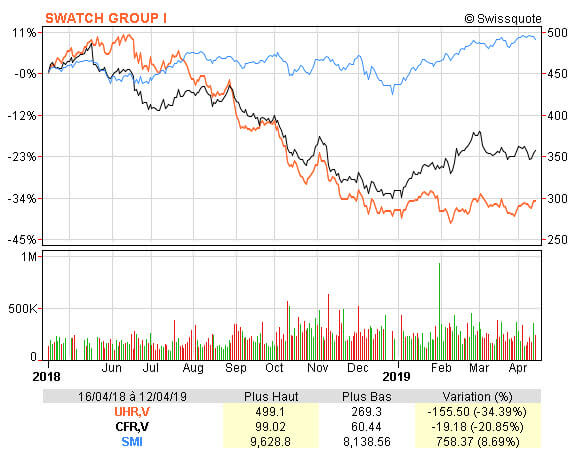

Comparative evolution since April 2018 of Swatch Group (orange curve), Compagnie Financière Richemont (black curve) and of the SMI (blue curve), the Swiss Stock Exchange's blue chips index

Swatch Group is struggling to convince investors. Its share price has been virtually flat since January, after losing 42% over the last seven months of 2018. Richemont, in comparison, is making headway. Meanwhile, French luxury groups are flying high.

These days, the higher up the luxury ladder groups are positioned the better, in investors’ eyes. Or so it would seem from an analysis of luxury players’ stock performance over the past year. The first takeaway is that French luxury multinationals, all of which operate a wide range of activities, are performing well. Buoyed by excellent results in 2018 and an optimistic outlook for the coming months, their share prices are soaring. LVMH shares increased by almost 30% over a year, and reached a record high in early April 2019. The same goes for Kering. Also in early April, Hermès shares came close to their highest ever level, achieved in May 2018, after gaining 29% since January. For certain financial analysts, the share is clearly overvalued on a price to earnings ratio of 43 (versus a sector median of 22), i.e. an 82% premium to rivals. All of which suggests Hermès has found the right business model.

The picture is less rosy where Swiss watch groups are concerned, in particular Swatch Group. The company led by Nick Hayek, which severed ties once and for all with Baselworld when it held its own fair in Zurich last March, has seen its shares struggle, losing 42% of their value between June and December 2018 on the back of sluggish international markets during the second half of the year. This decline has since been reversed although shares have yet to rally, gaining a timid 3% since January. Despite a 6.1% rise in net sales to CHF 8.5 billion and a 15.2% increase in operating result to CHF 1.15 billion in 2018, the group is having a hard time convincing investors. Alarm bells tinkled when inventory was lifted to close to CHF 7 billion. Next came news of production bottlenecks at the group’s two main brands, Omega and Longines, believed to have “cost” around CHF 200 million. Did USB investment bank have the right intuition? In November 2018, it issued a recommendation of Sell with a 12-month price objective down from CHF 410 (price at end August 2018) to CHF 272 – a more than 30% drop. As it turns out, shares plunged even before then, hitting their lowest ever point for the year in February at CHF 269.

"Neutral" for Richemont

Morgan Stanley is another financial establishment to have reservations about Swatch. In the second half of 2018 it downgraded the group’s rating to Underweight – a recommendation confirmed in its recent analysis of the Swiss watch market, published mid-March. Why such a judgement? Firstly due to 2019 estimated sales. The American investment bank anticipates no likely pick-up in sales with a corresponding drop in earning capacity. In view of cost inflation within the group, it estimates that Swatch Group would need to achieve 3% growth at constant exchange rates in order to post a flat margin – which is more than expected. Furthermore, Swatch Group is significantly exposed to the low-end segment (under CHF 3,000 wholesale) where competition from smartwatches is toughest. Other black spots, according to Morgan Stanley, are the time it will take to clean up the distribution channel and the group’s heavy reliance on its Omega and Longines brands, which generated around 70% of its operating profit in 2018.

In comparison, Richemont, which is positioned almost exclusively at the high end of the market, gets a more favourable review – a point of view reflected in the close to 16% increase in its share price since January, after tumbling 29% in 2018. Jewellery sales, which maintain operating margins in excess of 30%, and Cartier’s successful repositioning, particularly in China, are two of the group’s strong points underscored in the Morgan Stanley report, especially now that investor sentiment regarding the Chinese economy has significantly improved compared with end 2018. There are some clouds on the horizon nonetheless, such as the impact of foreign exchange movements, higher gold prices, and the positioning of Richemont’s YNAP and Watchbox online platforms. Watch this space until May 17th and the publication of Richemont’s 2018/19 annual report. Until then, and bearing in mind that sales by the group’s watch brands grew by just 1% over nine months versus a 9% increase for its jewellery Maisons, including Cartier, positive impacts on share prices aren’t to be excluded.

{kind=link}

{kind=link}

{kind=link}

{kind=link}