Traditional mindsets still prevail among Swiss watch brands

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

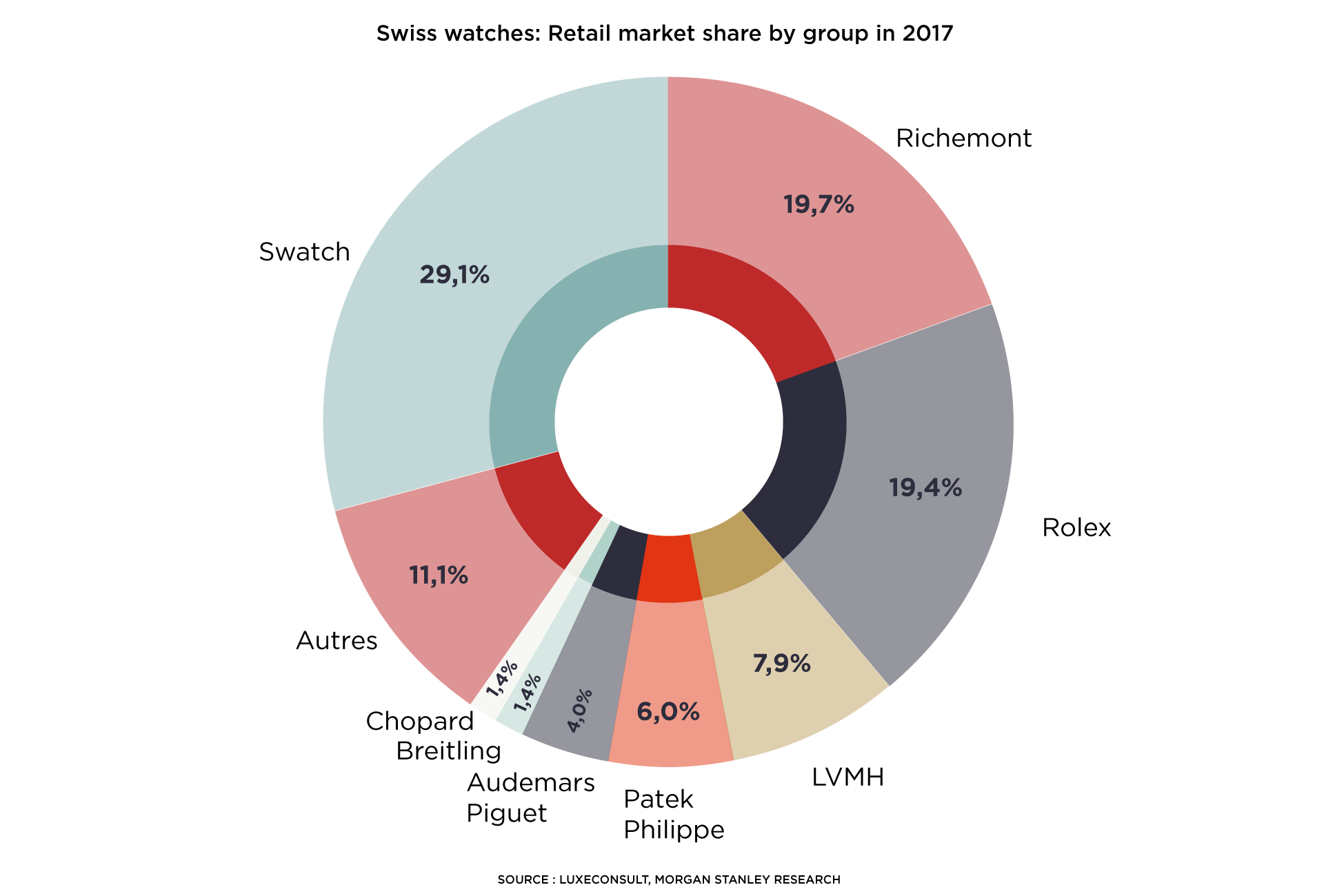

Just four groups account for around 75% of Swiss watch sales. A recent analysis of the sector by Morgan Stanley, in consultation with LuxeConsult, pinpoints an industry that operates on mainly traditional lines. How much longer can watchmakers continue to opt out of the digital world?

It’s official: Vontobel is no longer the only bank shedding light on the Swiss watchmaking economy. American investment bank Morgan Stanley recently published its analysis; a report that makes for obligatory reading, given the sparsity of information from a branch that likes to keep its finances under its hat. After detailing the estimated market share and financial weight of the main brands (see “Mega brands” rule the Swiss watch market), the American bank turns its attention to how Swiss watches reach the paying customer. Its opinion of the prevailing business models can be summed up in just a few words: traditional, not to say conservative. “Today, high end watches are more exposed to the wholesale channel than any other luxury goods sub segment.” The report goes on to note that 13 of the top 15 watch brands (the exceptions being Cartier and the Swatch brand) generated more than half their sales at wholesale, i.e. via third party retailers.

Leading brands such as Rolex and Patek Philippe make as much as 99% of their sales at wholesale. Morgan Stanley reminds readers that Patek Philippe operates only three of its own stores, or “Salons” as it calls them, in Geneva, Paris and London. Both Patek and Rolex have mono-brand stores in countries including the United States, United Kingdom, Canada, Australia and China, but these are franchises and therefore classified as wholesale. Even the industry’s two giants, Swatch Group and Richemont, rely heavily on wholesale despite efforts made over the past 15 years or so to expand their retail networks. By way of example, Morgan Stanley estimates that Vacheron Constantin (Richemont) made 25% of its 2017 sales at retail. At end March 2017 the brand operated 63 own-name stores; however, deduct sales made at the 32 franchises, and less than 15% of Vacheron Constantin watches (in value) were actually sold in the Richemont network. What’s true for the big names is even truer for the smaller brands that don’t produce sufficient volume to open an own-name store on one of the world’s famous shopping streets. Morgan Stanley concludes that an estimated 90% of Swiss watch sales in value are made via third-party retailers. This puts the Swiss watch industry in a unique position compared with other luxury segments such as leathergoods (40%) and jewellery (30%).

The importance of e-commerce

According to Morgan Stanley, there are two main reasons why watch brands should, in theory at least, be encouraged to develop their e-commerce. The first and most obvious concerns the sector’s very high gross margins, not only in relative terms (%) but also in absolute terms: when a customer buys a watch for €10,000, the average retailer mark-up is €4,000. This is mainly the result of high capital intensity and low inventory turnover (inventory remains in stores for an average of 250 days compared to 30 days for supermarkets), plus high – not to say prohibitive – real estate costs. The second reason is that stores can only carry a small part of brands’ collections. For example, a multi-brand store would be hard-pressed to show more than fifty or so of the 1,600 SKUs offered by Omega; that’s just 3% of the range.

In these circumstances, the American bank sees no reason why Swiss watchmaking should remain on the sidelines of e-commerce, particularly now that online sales are accounting for an ever-increasing share of purchases in every segment. The industry still balks at what it sees as dissuasive barriers, for example fear of counterfeits and the instinctive need to belong to a physical world – the famous “touch and feel” factor. Morgan Stanley estimates no more than a 5% penetration for online sales of Swiss watches. But, it says, “the dam has now broken”. Significant changes are taking place. Watch platforms are gaining ground, having succeeded in reassuring customers as to the authenticity of products sold online. Morgan Stanley gives the example of Chrono24. The site, which is also supplied by retailers, lists more than 400 brands and carries over 335,000 watches at any one time. Something no brick-and-mortar store can hope to match.

The spectre of the grey market

Price disparities are an additional factor that has helped boost the development of these online platforms. Foreign exchange rates must always be taken into account – remember how the post-Brexit drop in sterling’s value promoted the United Kingdom to the fastest-growing European market for Swiss watches in 2016 and again in 2017. Morgan Stanley suggests that the arrival of online platforms has accentuated the grey market – always part of the equation due to the wholesale nature of the Swiss watch industry – and increased its impact on distribution overall, mainly as a result of foreign exchange. The report cites the United States as an example. Swiss watch shipments to the US have fallen significantly over recent years, dropping 28% in volume and 14% in value between 2014 and early 2018 – the biggest decline ever for the market over the past century. Morgan Stanley’s analysis of the situation concludes that this unprecedented shortfall is due to the US dollar’s strong appreciation against the euro and the yuan, prompting Chinese and European retailers to offload excess inventory to platforms selling to US customers. A theory borne out by the fact that Swiss watch shipments to the United States rose by 28% in February 2018 (the biggest monthly upswing since March 2012), following a continuous depreciation of the dollar against the main global currencies over the previous months.

Not having an online presence equates to abandoning the online channel to grey market players.

Morgan Stanley

For Morgan Stanley, there can be only one conclusion: “Not having an online presence equates to abandoning the online channel to grey market players. With millions of potential customers around the world now enquiring online about Swiss watches, we can bet with relatively certainty that these same potential customers, looking to purchase watches, are checking availability and prices online.” Hence why brands are starting to react, for example through partnerships and commercial collaborations with platforms, information sites and blogs, when they aren’t launching their own transactional websites – mainly focused on the United States for the time being. Not everyone shares their enthusiasm for online channels. Meaning more to gain for those that do?