Watch industry execs see more good things to come

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

W

The latest study by Deloitte of the Swiss watch industry, published in September, reveals that senior executives are optimistic for future growth.

Swiss watch exports have posted a marked slowdown yet confidence among the industry’s executives remains intact, an optimism shared with the Federation of the Swiss Watch Industry. Its latest analysis notes that “July reached new highs in terms of watch exports, with the result exceeding the CHF 2 billion mark. This level has never been reached so early in the year before. July thus becomes the fourth best month on record.” Yet the fact remains that from January to July 2013, cracks appeared in the industry’s formidable progression: exports increased 1.1% compared with the same period 2012, when exports gained 11% for the year as a whole, after rising 19.4% in 2011.

High-end leads the way

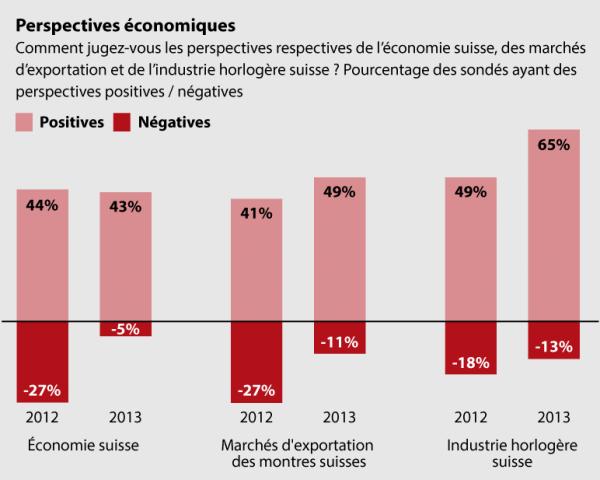

The second , published early September, nonetheless leaves no doubt as to the industry’s upbeat mood. Of the 53 senior executives interviewed, 65% have a positive outlook for the Swiss watch industry over the next twelve months compared with 49% the previous year. While demand has slowed in China, they believe that other emerging markets, as well as the United States, will take up the slack. Sales to tourists, particularly in Switzerland and European Union countries, are also expected to further drive results.

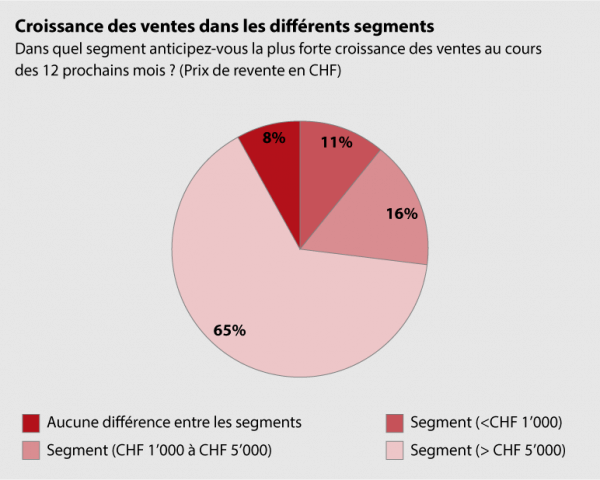

“Key features of this year’s survey show industry executives being the most optimistic for growth at the high-end of the watch market,” writes Howard da Silva, Consumer Business Leader at Deloitte. Indeed, two-thirds of respondents expect the industry to perform best in the segment of watches priced above CHF 5,000, although export figures for the first half-year 2013 show that entry-level watches fared better than other segments in both quantity and value.

Inevitable verticalisation

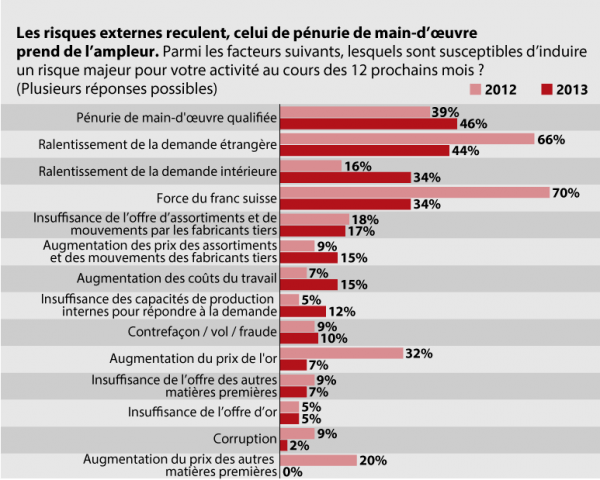

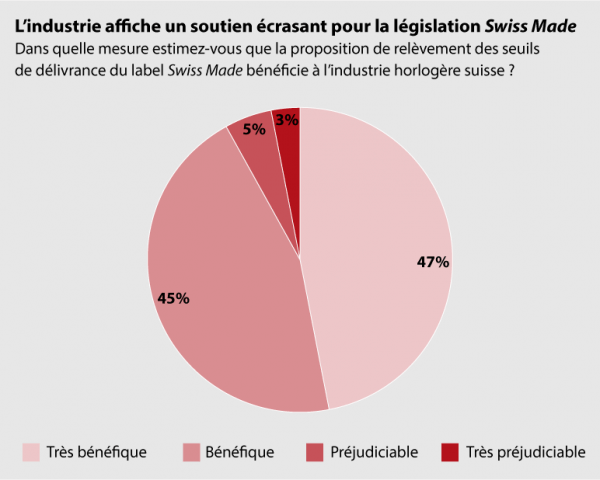

The Deloitte study also highlights a shift in concerns. Last year, 70% of respondents cited the strong Swiss Franc as their biggest perceived risk, just ahead of weaker foreign demand (66%) and the rising price of gold (32%). This year, their main concern is a shortage of qualified labour (46%), closely followed by the slowdown in demand from international markets (44%). While 92% of those questioned support tougher Swiss-Made legislation, and despite broad approval for the decision taken in July by COMCO (Switzerland’s competition watchdog) that Swatch Group should renegotiate its gradual reduction of movement and parts supplies, more than 40% fear that these two factors could lead to supply-side difficulties. Some even anticipate that brands which are over-dependent on outside suppliers could disappear.

Increased verticalisation of distribution channels is also perceived as a threat, particularly for smaller independent brands. Unsurprisingly in this light, two-thirds of respondents came out firmly in favour of maintaining a network of independent local distributors. Further vertical integration is nonetheless inevitable according to the 79% who believe the spate of mergers and acquisitions is far from over, driven by the need to secure sourcing and qualified labour. Meanwhile, the overwhelming majority of surveyed executives (91%) view innovation as a major asset for the industry, while 88% are convinced that social media have a vital role to play. As Deloitte concludes, “the main sentiment from Swiss watch executives is one of confidence that their industry will continue its extraordinary success story.”