What the numbers say

close

Franco Cologni

President of the FHH Cultural Council

CLOSE

January marks the end of holiday festivities; for watchmaking too, the party’s over.

With January come figures for 2016. The only serious quantitative reference – and even then to be handled with caution – is published by the Federation of the Swiss Watch Industry (FH).

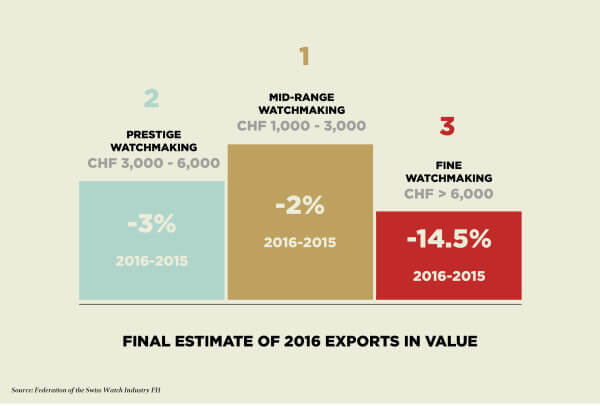

Looking back over my notes and adding data for December 2015 – when the current crisis was already being felt – to figures for the past eleven months, I observe a 10% drop in units sold (25 million) and a 9.5% fall in revenue (CHF 18 billion). With, of course, significant variations per export price category (

In truth, these statistics do not reflect the situation in the markets; other than estimates, we have no reliable data concerning actual sales. It is my belief, and that of recent articles in the press, that sales to end customers have been less, possibly substantially less, than exports insofar as this downturn equates to surplus inventory together with products re-imported by the manufacturers.

Put bluntly, everyone from analysts to journalists will be sinking their teeth into figures that can give no meaningful indication of what we experienced last year. A situation which, as I said, was largely predictable.

A few words on Fine Watchmaking (>CHF 6,000), Prestige Watchmaking(CHF 3,000-6,000) and Mid-Range Watchmaking (CHF 1,500-3,000). These segments are of particular interest not because they were the year’s top-selling categories, but because their sales were least impacted by the crisis.

Working from the top…

– Watches in the over CHF 6,000 category dropped a worrying 14% in value to around CHF 8 billion, which puts this segment third out of the three under scrutiny here (having been top of the leader board for the previous five years).

– Better news in the CHF 3,000-6000 category which fell by less than 3% to some CHF 4 billion. This segment is weathering the storm and takes second place on the podium.

– Watches in the CHF 1,500-3,000 category show an even softer decline. Having lost 2% to CHF 2 billion, this category claims first place.

These three price points, which account for considerably more than 75% of total exports, form two subgroups. The first – watches with an export value over CHF 6,000 – is in sharp decline whereas the second – watches with an export value between CHF 1,500 and CHF 6,000 – is in a consolidation phase.

There can be no eluding the fact that what we refer to as technical and precious Fine Watchmaking has taken a punch. I’ll leave it to the profession to understand why. My opinion is that the euphoria of recent years translated into price increases that were out of touch with the value of the product. Making matters worse, everyone was drunk on success and lost sight of the values on which Fine Watchmaking is built: identity, authenticity, relevance, singularity, originality and innovation.

It is the product itself, at a fair price, which can become an icon whose fortunes are in the hands of history.

The party’s over. We have returned to 2011 levels. But the world does change after all, and a little self-criticism never did anyone any harm if it helps safeguard the qualities required to hold on to an increasingly coveted first place. The upcoming SIHH in Geneva will tell us whether we have learned our lesson from 2016 and whether we can set off anew, not dazzled by illusions but with a great deal of perseverance. From now on, marketing and communication do not make the product; instead, it is the product itself, at a fair price, which can become an icon whose fortunes are in the hands of history.

*The generally accepted rule is that retail price excluding local tax is export price multiplied by 2.5 or 3.

{kind=link}